- "Buy now pay later" is growing in popularity among younger consumers especially for online shopping, and an increasing number of companies have started offering the service in the past couple of years.

- Many such BNPL providers do not report the use of such services to credit bureaus, Fitch Ratings said.

- This trend could cause consumer debt and credit card balances to spike, analysts warn.

"Buy now, pay later" options are becoming increasingly popular, but analysts warn of default risks given the lack of credit checks and "opaque" debt reporting.

Not being able to check on consumers' credit history could lead to lenders to underestimate borrowers' debt levels when assessing new loan applications, they said. There's also the risk of consumers chalking up more credit card debt in order to pay off their "buy now, pay later" (BNPL) obligations, analysts warned.

BNPL providers usually tie up with retailers — both online and in stores — to offer consumers the option to pay in installments, with perks including no late fees and often high loan limits.

Get DFW local news, weather forecasts and entertainment stories to your inbox. Sign up for NBC DFW newsletters.

Such payment options are growing in popularity among younger consumers especially for online shopping, and an increasing number of companies have started offering the service in the past couple of years.

The sector came under the spotlight last week when digital payments company Square announced a $29 billion deal to buy Australia's "buy now pay later" provider Afterpay.

Money Report

Default risks

In a recent report, Fitch Ratings said the sector's debt performance reporting is "opaque." Many such providers do not report the use of such services to credit bureaus, the ratings provider said.

"Consequently, BNPL debt is often not visible on the credit file and borrowers could try to get BNPL credit from multiple providers," Fitch analysts wrote. "Lenders (including non-BNPL) could underestimate a borrower's debt level when underwriting new debt."

Stephen Biggar, director of financial institutions research at Argus Research warned that defaults are "one of the primary risks."

"These companies are not doing any kind of credit background check on these individuals," he told CNBC's "Squawk Box Asia" last week. "During a downturn, they may be the first to buy now and not pay later."

How 'buy now, pay later' works

Traditionally, installment plans have been offered in stores for decades. However, it used to be typically for big-ticket items such as furniture, electronics and household appliances that cost thousands of dollars.

The latest "buy now, pay later" plans straddle a segment between credit cards and instalment plans. Focusing on younger and more tech-savvy users, they are offered for online purchases that can be as low as $10 to $20, or as high as thousands of dollars.

Among the more popular providers is U.S.-based pay-over-time company, Affirm. The maximum value that can be taken out on a single payment plan with Affirm is $17,500.

A lot of these financial technology apps offer sweeteners that credit cards and traditional installment plans don't — they sometimes include no late fees, low or no interest, high loan limits and no credit checks required. The conditions vary across providers.

On the flip side, the costs of borrowing can spiral if consumers don't read the conditions carefully.

There are some potential pitfalls in fine print: additional fees such as extra charges for rescheduling payments, and some providers charge high late fees.

Analysts also warned of the propensity for spontaneous purchases given the simplicity of the application process and cheaper costs of borrowing compared to credit cards.

Usage of such payment options shot up during the pandemic as online shopping surged, Fitch said.

In the U.S., these short-term installment-like loans saw a 215% jump year-on-year in the first two months of this year, according to data from Adobe Analytics. Consumers using such services placed orders that are 18% larger compared to the same period in 2020, the data showed.

The volume of U.S. e-commerce payments made using BNPL rose to $19 billion last year — more than double the $9.5 billion spent in 2019, Fitch said, citing estimates from payments company Worldpay.

Providers that have surfaced in this segment include Affirm, Quadpay and Klarna.

More established financial companies have jumped on the bandwagon too: PayPal, Mastercard, American Express, Citi and J.P. Morgan Chase are all offering similar loan products, while Apple is reportedly looking to offer such a service as well.

Credit card debt could shoot up

Fitch warned that such "buy now, pay later" debt could rack up and even spill over to credit card debt.

"BNPL users may find themselves unable to afford the periodic repayments and may turn to credit cards or other forms of high interest debt to repay BNPL debts," it said.

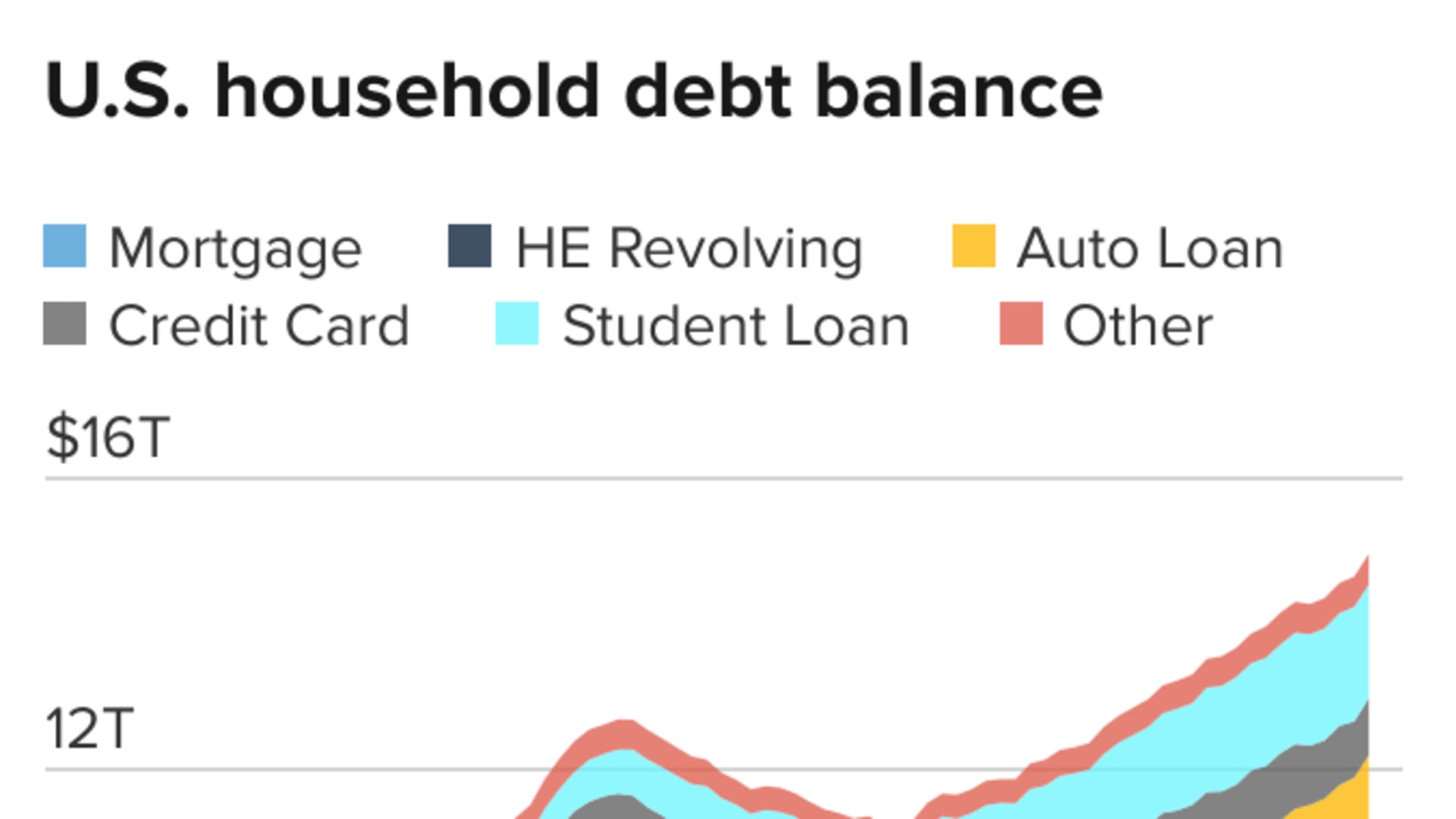

U.S. household debt rose by its highest dollar amount in 14 years during the second quarter, according to the Federal Reserve. While that was mostly due to a surge in the housing market, credit card balances also jumped $17 billion from the first quarter — to a total of $787 billion.

According to Fitch, findings by the Australian Securities and Investment Commission in November showed that 15% of Australian consumers using such pay-later schemes had to take out an additional loan in the previous year to pay off their BNPL plan on time.

In the UK, Fitch cited a major UK bank which reported that of its over 660,000 customers who paid their BNPL providers, 10% exceeded their overdraft limit in the same month.

Biggar of Argus Research told CNBC that in the past quarter, transaction losses for Square "went up significantly."

According to Square's 2019 annual report, transaction and loan losses for the year ending Dec. 31, 2019 widened by 44% compared to the previous year.

On the risks of consumers missing payments, he said: "That is definitely a concern, as we look out into the next possible downturn ... these loans have to be backed by something."

In comparison, credit cards have "safety" features built-in, including cutting off access to the card, he pointed out.

— CNBC's Jeff Cox contributed to this report.