- Why was the pause extended? Should you continue skipping payments?

- Here's what student loan borrowers need to know about the latest extension of the payment pause and interest waiver.

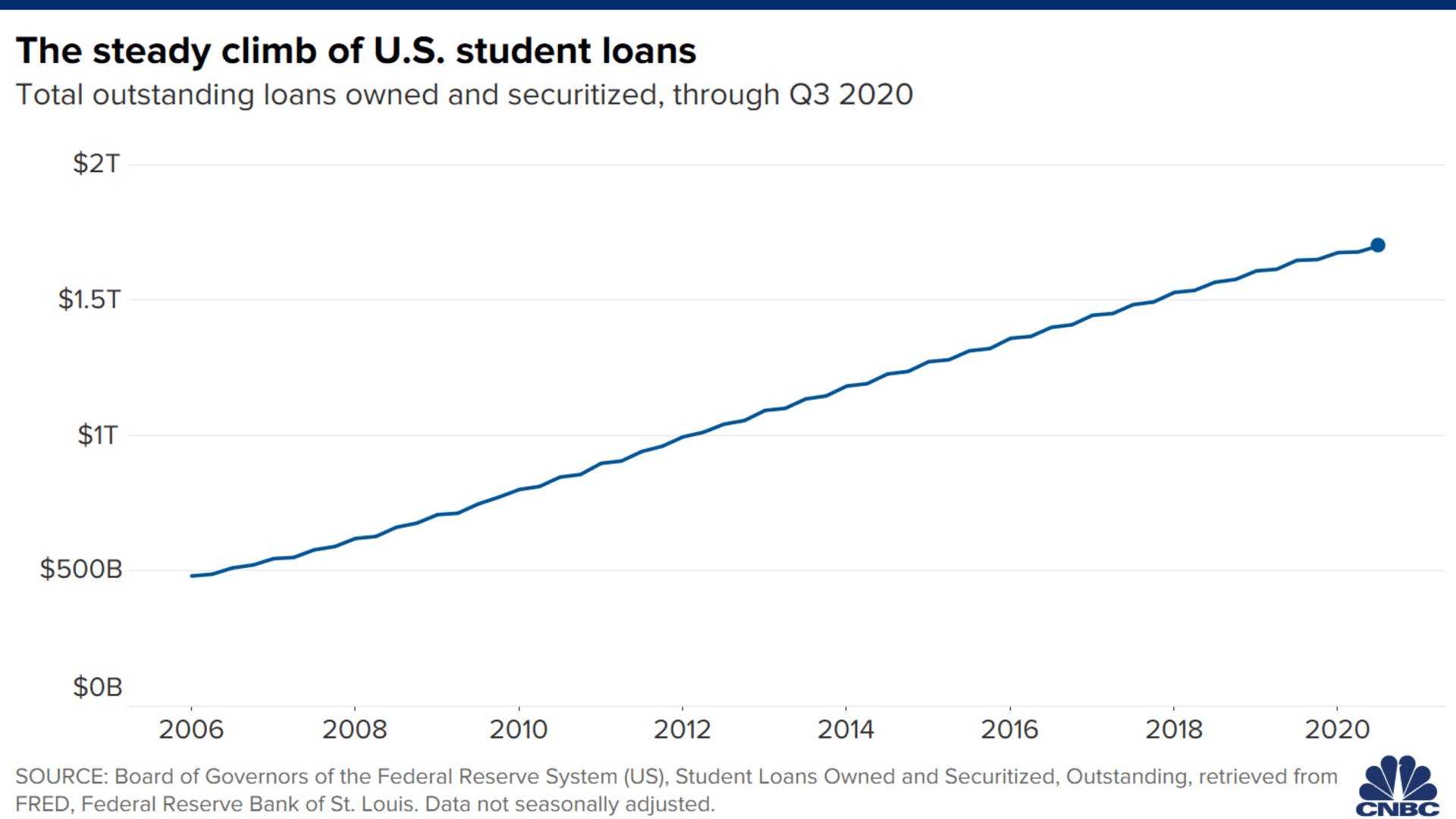

Federal student loan borrowers have another six months before they'll need to start making their payments again, thanks to an announcement by the White House last week.

The payment pause and interest waiver on federal student loans, which more than 40 million Americans hold, has been in effect since March 2020, when the coronavirus pandemic first hit the U.S.

After several extensions, borrowers now don't have to worry about their bills until next February. In the meantime, here's what you need to know.

Get DFW local news, weather forecasts and entertainment stories to your inbox. Sign up for NBC DFW newsletters.

Why was the payment pause extended again?

There are likely a few reasons the Biden administration decided to give borrowers more time. For one, it was under pressure from Democrats to do so.

"Since the beginning of the Covid-19 pandemic, millions of Americans have struggled to keep a roof over their heads, pay bills and put food on the table," the heads of the Senate and House Education Committees, Sen. Patty Murray, D-Wash., and Rep. Robert C. Scott, D-Va., respectively, wrote to the White House in June.

Money Report

"While the economy has begun to show promising signs of recovery, more than 9 million Americans remain out of work, and the economic and health disparities created by the pandemic are severe."

Indeed, unemployment levels among young workers are still higher than they were before the public health crisis. And in a recent survey conducted for The Pew Charitable Trusts, more than 66% of student loan borrowers said they're not ready to start their payments again.

Lastly, a recent change in student loan servicing may have worked in borrowers' favor.

The Pennsylvania Higher Education Assistance Agency — which oversees the loans of 8.5 million student borrowers — announced last month that it would not renew its contract with the federal government when it ends in December. As a result, those borrowers will need to be matched with a new lender.

The U.S. Department of Education likely didn't want to force these borrowers to begin repayment and then have to change their servicer two months later.

"It would be better to combine both changes so that they occur at the same time," said higher education expert Mark Kantrowitz.

Should I keep not paying?

There's no harm in taking advantage of the government's payment pause and interest waiver. When your bills resume, your debt shouldn't be any higher.

"It is as though their loans were in hibernation," Kantrowitz said.

If you're pursuing public service loan forgiveness or are on an income-driven repayment plan, it may be a bad idea to continue making payments. That's because those months of the payment pause count toward the eventual debt forgiveness these programs lead to — whether or not you're paying. So any money you direct to your loans during this reprieve just reduces the amount of forgiveness for which you'll be entitled.

More from Personal Finance:

How stimulus checks changed Americans' ability to cover emergencies

Early end to federal unemployment pay not getting people back to work

Are you protected under the new eviction ban? How to figure that out

But for borrowers in the standard repayment plan who can afford to do so, it may make sense to continue making payments. Because interest is suspended at the moment, your money will go right toward the principal and your debt will shrink faster.

Still, others may want to use this time to tackle other debt with higher interest rates, such as a mortgage or balances on a credit card.

What if I was in default?

If you were in default and working to rehabilitate your loan, you're in luck. That's because the Education Department's rehabilitation program requires nine consecutive on-time payments, and the months during the payment pause count toward this process, whether or not you made a payment. Depending on when you started rehabilitation, your loans may already be out of default. The payment pause has now been in effect for 16 months.

If you weren't in the rehabilitation process, collection activity may resume come February. To avoid that, experts recommend reaching out to your servicer and asking about the process of getting current.

During the payment pause, defaulted borrowers are protected from garnishments of their wages, Social Security checks and tax refunds.

What can I do about my private student loans?

Private student loans, of course, aren't eligible for the government's break.

If you're struggling, experts recommend reaching out to your lender to see what accommodations may be available to you.

Could the payment pause be extended again?

The Education Department said this would be the "final extension" of the respite, which has now been in effect since March of last year.

Still, experts say a lot depends on the state of the pandemic and economy come February.

If you're still unemployed or dealing with another financial hardship because of Covid, you'll have options whenever payments resume.

Applying for an economic hardship or unemployment deferment will allow you to postpone your payments without interest accruing. If you don't qualify for either of those, you can still use a forbearance to continue suspending your bills.

For those who expect their struggles to last a while, it may make sense to enroll in an income-driven repayment plan. These programs aim to make borrowers' payments more affordable by capping their monthly bills at a percentage of their discretionary income and forgiving any of their remaining debt after 20 years or 25 years.

Is student loan forgiveness still on the table?

Yes.

Biden has asked the U.S. Department of Justice and the U.S. Department of Education to review his legal authority to forgive student debt through executive action. The fact that those reports are still pending may explain why we haven't heard anything more definitive yet.

"He's not going to take any steps until that report comes back," Kantrowitz said.

Legal experts and other Democrats insist that the president has the power to cancel student debt without Congress. "All you need is the flick of a pen," Senate Majority leader Chuck Schumer, of New York, has said.

Even if government officials conclude that Biden doesn't have such authority, there could still be hope.

Although Democrats might find it hard to pass legislation forgiving student debt in Congress, given their razor-thin majority, they could turn such a bill into law though the budget reconciliation process in the fall. That avenue wouldn't require the support of Republicans.