The NBC 5 Responds team has helped consumers navigate more than a few storms. Find out what to know before, during and after damaging weather.

The NBC 5 Responds team has helped consumers navigate more than a few storms. Read on for what to know before, during and after damaging weather.

UNDERSTANDING CURRENT COVERAGE

Before bad weather strikes, take steps to minimize a financial hit later. Pull out your insurance policy and read it. You can start with the first page or two, known as the “dec page” or declarations page. This summarizes your policy and deductibles. Brush up on what’s covered and what’s not.

For example, liability auto coverage wouldn’t cover repairs to your vehicle if it’s damaged by hail or a falling tree branch. Damage caused to your vehicle by something other than a collision would fall under comprehensive coverage.

Get DFW local news, weather forecasts and entertainment stories to your inbox. Sign up for NBC DFW newsletters.

For your home, understand if you have actual cash value (ACV) or replacement cost value coverage (RCV). As the state’s Office of Public Insurance Counsel explains, ACV pays less than replacement cost value coverage because it subtracts for factors like age and wear and tear. For example, if a roof is a few years old, ACV coverage factors in depreciation when insurance pays the claim.

You may have bought replacement cost value coverage, but some items may only get paid at the actual cost value. That may include the roof.

Read your policy, including renewal paperwork to evaluate your insurance coverage and needs.

Local

The latest news from around North Texas.

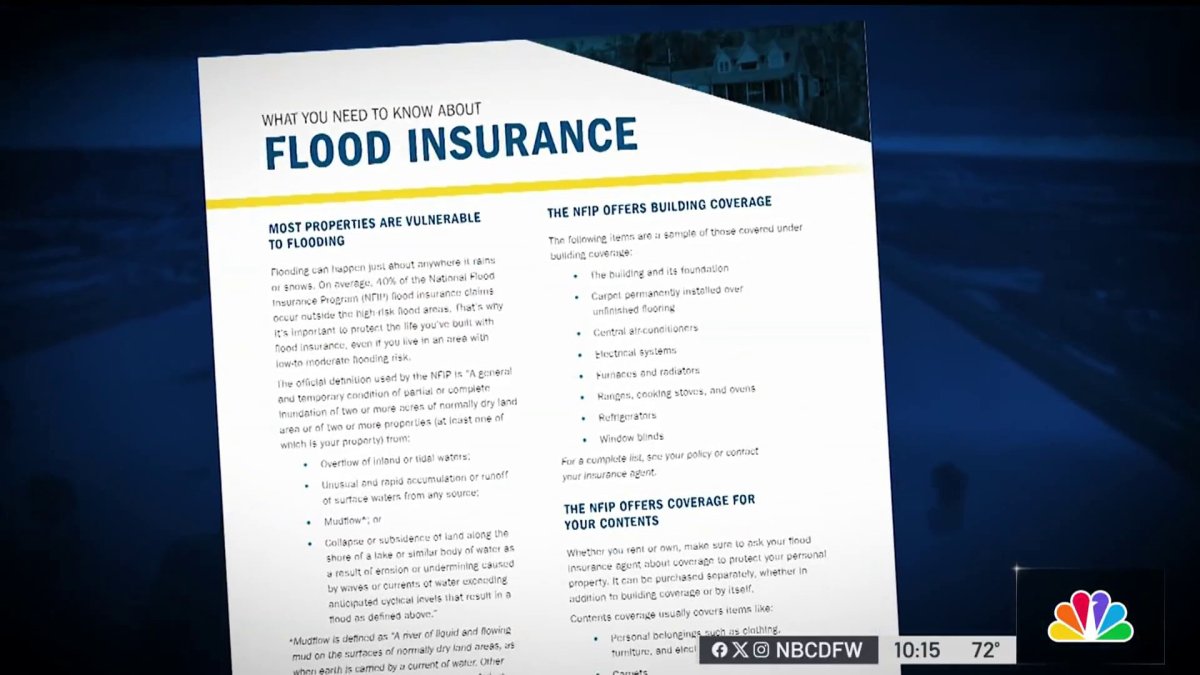

FACTS ABOUT FLOOD INSURANCE

Standard homeowners and renters insurance policies do not cover flood damage. Consumers would have to purchase separate insurance, typically from the National Flood Insurance Program, administered by FEMA.

In some places, considered high-risk, flood insurance may be required by the mortgage lender. However, flash flooding could happen anywhere. On average, around 40% of NFIP claims come from outside high-risk flood zones.

As Gilbert Giron, regional flood insurance liaison with FEMA Region 6 has explained to NBC 5 Responds, “At no time will you find anywhere on those maps that this area will not flood. There's always a risk.”

Note that homeowners and renters without flood insurance may not be able to fall back on federal disaster help. The president would have to declare a disaster. Individual assistance, in those disaster zones, would be limited to minimal repairs needed.

Consumers can check with their current provider about buying a flood policy or search floodmart.gov.

Most policies have a 30-day waiting period before kicking in.

NAVIGATING CLAIMS FOR DAMAGE

If you have to file a claim, contact your insurance provider as soon as possible. Document what happened, save receipts for emergency repairs and preserve evidence of damage.

This could be pieces of a carpet, damaged tile or window treatments. The insurance adjuster may ask to inspect the type and quality of the materials you had - which could impact what’s paid for your claim.

Keep a log of your interactions with the insurance provider and adjuster. Note who you spoke with, when and what was discussed. As Ware Wendell with Texas Watch has explained to NBC 5 Responds, some communication may be verbal. If that’s the case, ask for an email address for your contact at the insurance company. After every conversation, follow up with an email, highlighting what was discussed.

When an insurance company sends an adjuster to check the damage, ask if they’re an independent adjuster hired by your insurance company. That wouldn’t be unusual after a big weather event.

Ask if they are authorized to make the decisions about your claim. If not, find out the name of the in-house adjustor with your insurance company.

CREATE A HOME INVENTORY

Have you done a home inventory? It only takes a few minutes and can help a consumer navigate an insurance claim later. A home inventory documents the condition of your home and the contents inside.

Use your smartphone to take a video tour of your home. Be sure to open closets and drawers. Capture model and serial numbers of high-value items. Save your home inventory to the cloud or email it to yourself for safekeeping. Do this regularly, every time you move and when you make a big purchase for the home.

The TDI has a checklist to help you get started. There are free apps online. Your insurance company may offer a home inventory checklist too.

STARTING REPAIRS

If you have to hire someone to make repairs after a storm, understand Texas does not require state-level licensing for roofers and general contractors. It’s up to consumers to check them out.

Research how long the company has been in business under the same name. Are you seeing complaints in online searches? How is the company responding?

Request references of past work and call those references. Ask for proof of general liability insurance coverage. You can contact the insurance provider to confirm the contractor’s policy is current.

After a storm, you may need someone to get started quickly to prevent further damage.

Karen Vermaire Fox with the North Texas Roofing Contractors Association has told NBC 5 Responds, consumers should pause just long enough to do homework on the company or contractor.

“If you have a leak, if there's something wrong, you want to get that tarped, but that doesn't mean you have to go to construction right away,” Vermaire Fox explained.

The consumer may pay for materials to start the work but don’t pay for the entire repair in full, up front.

Apply skepticism if someone shows up at your door, promising steep discounts on a big repair job.

NBC 5 Responds is committed to researching your concerns and recovering your money. Our goal is to get you answers and, if possible, solutions and a resolution. Call us at 844-5RESPND (844-573-7763) or fill out our customer complaint form.

Get DFW local news, weather forecasts and entertainment stories to your inbox. Sign up for NBC DFW newsletters.